Debt Validation 2026:

The Complete §809(b) Framework

Last Updated: April 2026

A collection letter just arrived. The next 30 days will determine whether you pay whatever they demand, pay nothing because they can't prove you owe it, or collect damages from them for violating the law.

This guide is your 30-day playbook. The Regulation F checklist. The validation letter template. The documentation protocol. The FDCPA violation menu. And the recovery path if the 30 days have already passed.

Quick Answer: Does Debt Validation Work?

Yes. In March 2026, Washington State's Attorney General secured $6.2 million in debt erasure through validation failures alone. Collectors who cannot prove chain of ownership must stop collecting. Each violation of the validation freeze is worth up to $1,000 in federal court. The validation letter is not a suggestion — it is a legal instrument.

Section 1: The 30-Day Moment — Why It Defines Everything

The most powerful position in debt validation is pre-contact awareness. Before any collection letter arrives, consumers should understand: the 30-day clock starts from the date the validation notice is delivered, not the date of first contact. The collector has 5 business days from first contact to send the validation notice. Their failure to send it within 5 days is itself a violation.

Most collectors are banking on consumers not knowing any of this. They are professionals at cranking up the emotional volume so you cannot think clearly about the math. This framework exists to flip that equation.

The Three Scenarios — And Which One Applies to You

- You recognize the debt and the amount is accurate: Validation still matters — verify chain of ownership before paying. Debt buyers often cannot prove they legally own the account.

- You don't recognize the debt at all: Validation letter is mandatory immediately. This could be a scam, identity theft, or a collector pursuing phantom debt. Never pay without documentation.

- You recognize the collector but dispute the amount or accuracy: Validation is your primary weapon. Errors in principal, interest, fees, or the date of first delinquency are common — and each error is a potential FCRA violation.

The enforcement landscape has shifted. With CFPB enforcement at historic lows in 2026, consumers' own knowledge of §809(b) is now their primary protection. The agency that was supposed to police debt collectors is operating at reduced capacity — which means you are now the enforcement mechanism.

Before Anything Else: Pull Your 3-Bureau Report

The collection letter is the collector's version of events. Your credit report is the documentary record. You need both to understand what you're dealing with. What does the collection appear as on each bureau? What is the date of first delinquency? Is the amount consistent across bureaus?

Get Your 3-Bureau Report ($1 Trial)Affiliate link. We may earn a commission at no extra cost to you. See our disclosure.

Section 2: The Complete Legal Framework — §809(a), §809(b), and Regulation F

Every guide treats debt validation as a single action. The distinction between §809(a) and §809(b) is legally critical but absent from all consumer-facing content. ScorePivot's framework is the first to present this two-provision structure as actionable strategy.

The Two Provisions of FDCPA §1692g

§809(a): The Collector's Obligation

Within 5 business days of first contact, the collector must send you a written validation notice containing: the amount of the debt, the name of the creditor, and a statement that you have 30 days to dispute. This is their proactive obligation — they must do this without you asking. A collector who fails to send the §809(a) notice within 5 days has already violated the FDCPA before you do anything.

§809(b): Your Right to Trigger the Freeze

If you send a written dispute within 30 days of receiving the validation notice, all collection activity must cease until the collector provides proper verification. This is your affirmative right — you choose whether to exercise it. Once triggered, the freeze is legally binding. Each contact after your letter, before verification, is a separate violation.

What Regulation F Added in 2021

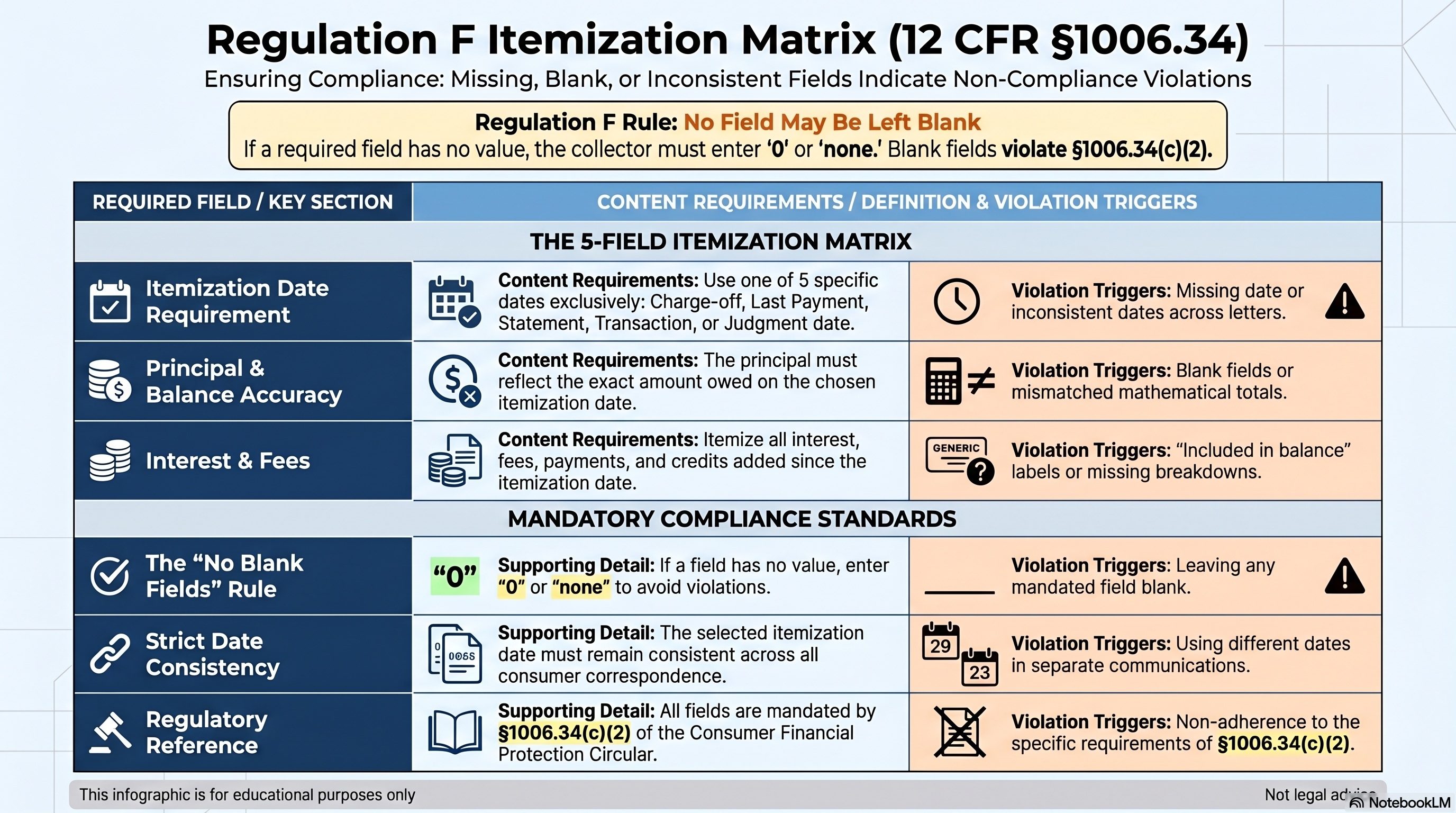

Regulation F is the CFPB's comprehensive debt collection rule implementing the FDCPA. It became effective November 30, 2021, and fundamentally changed the documentation requirements for collectors:

- Model Validation Notice: Collectors must use a specific format with required elements. Straying from the model creates areas of opportunity for plaintiff's counsel to challenge changes.

- Itemization Requirement: The notice must include an itemized breakdown of the debt — principal, interest, fees, payments, and credits since the itemization date. A missing itemization is itself a violation.

- Itemization Date Options: Collectors must choose one of five reference dates for the itemization. The chosen date determines how the balance is calculated.

- Electronic Communications Rules: Specific consent requirements for email and text contact, opt-out mechanisms in every electronic message.

- Time-Barred Debt Disclosure: If the debt is past the statute of limitations, the notice must disclose this on the front page.

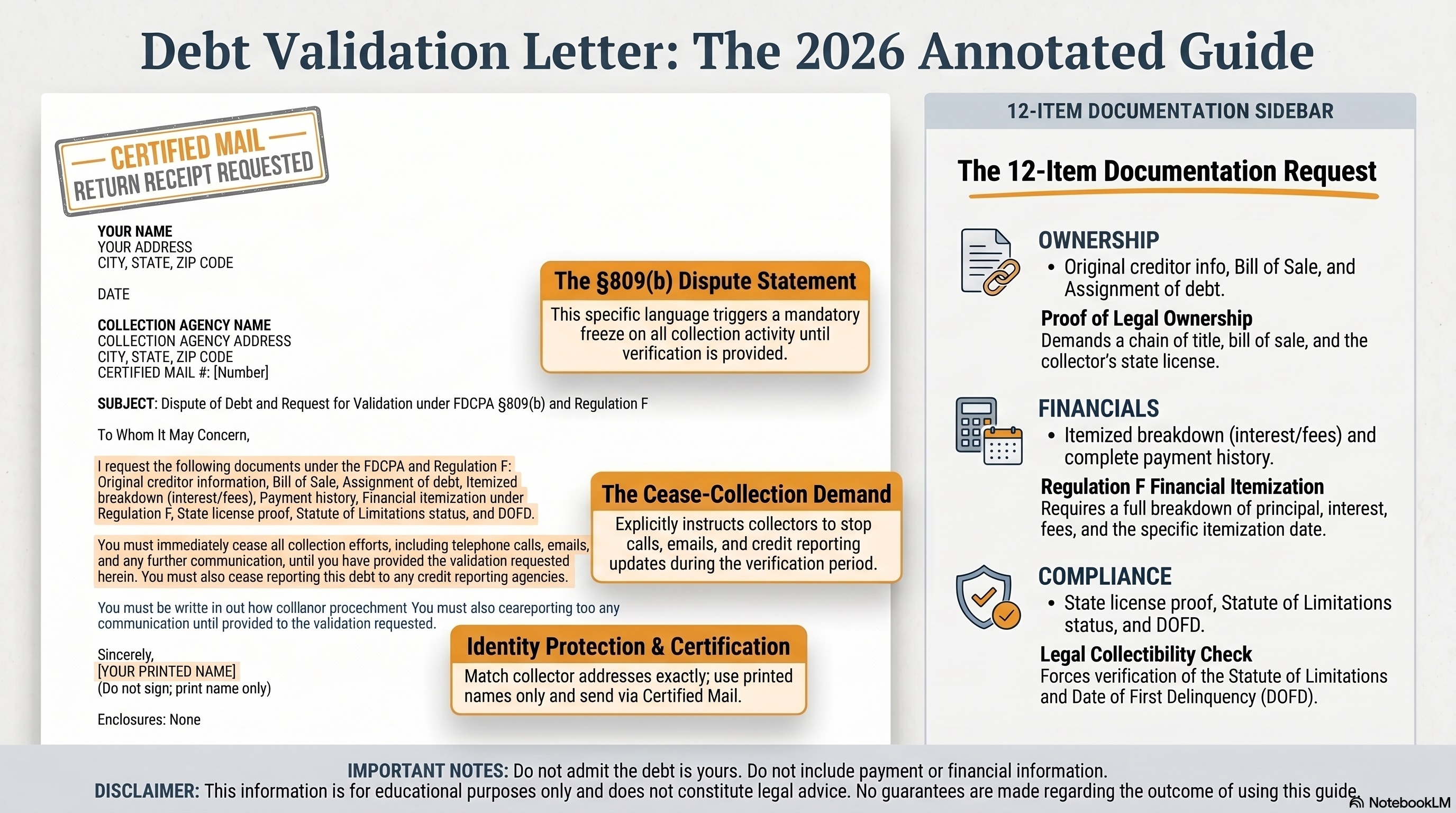

Figure 1: Debt Validation Letter: The 2026 Annotated Guide — Includes all required elements, the §809(b) dispute statement, cease-collection demand, identity protection certification, and the 12-item documentation request list.

The Validation Period Math

The 30-day window is calculated from the date you receive the notice, not the date it was mailed. Under the 5 business day delivery presumption, your actual window is typically 35 calendar days from the mailing date shown on the collector's letter. Calculate your deadline precisely — missing it by one day changes the legal landscape.

Section 3: Audit the Collector's Notice First

Before you send anything, audit the collector's validation notice for compliance. A deficient notice is an independent FDCPA/Regulation F violation that exists before you do anything. Check whether the collector violated §809(a) before you exercise §809(b).

Regulation F §1006.34 Compliance Checklist

The collector's notice must contain ALL of the following:

Missing any required element = potential Regulation F violation. If the itemization shows no interest or fees, that field must say "0" or "none" — it cannot be blank.

The CFPB emphasized that if other things are included with the Model Form B-1 that overshadow, conflict with, or confuse the consumer, the safe harbor for the Model Form B-1 can be jeopardized. Collectors who deviate from the model create opportunities for challenge.

The Scam Detection Function

Because debt collectors are now allowed to email, text, and use social media, scammers also use these channels to trick you. A validation letter serves two purposes simultaneously: exercising legal rights and exposing scammers. Scammers cannot validate because they have no documentation for debts that don't exist. If a "collector" cannot produce any documentation, you may be dealing with phantom debt fraud.

Before You Engage: Check the Dark Web

Scam collectors use real-sounding names and real debt amounts gleaned from data breaches. Before engaging with any collector, scan the dark web for your personal information. If your financial data is circulating, the "debt" may be a scam built from stolen information.

Scan for Data Breaches NowAffiliate link. We may earn a commission at no extra cost to you.

Section 4: Writing the Validation Letter That Works

The validation letter is the instrument that exercises your §809(b) rights. It must be in writing (verbal disputes do not trigger the freeze), sent within 30 days of receiving the validation notice, and sent via certified mail with return receipt requested (creates the documented proof of receipt that every subsequent legal claim depends on).

The 12-Item Documentation Request List

Your validation letter should request the following specific documentation. The more specific you are, the harder it becomes for collectors to respond with form letters:

- 1Name and address of original creditor

- 2Amount of the original debt and itemized breakdown of current amount

- 3Copy of the original signed agreement creating the debt

- 4Documentation of chain of ownership (bill of sale or assignment showing each transfer from original creditor to current holder)

- 5Proof of the current holder's license to collect debt in your state

- 6Date of first delinquency (the date from which the FCRA 7-year reporting clock runs)

- 7Statute of limitations status in your state

- 8Complete payment history showing all payments and credits applied

- 9Calculation showing how interest and fees were determined

- 10Proof that the statute of limitations has not expired

- 11Verification that this debt has not been discharged in bankruptcy

- 12Demand that all collection activity cease until valid verification is provided

What NOT to Include in Your Validation Letter

- Do not admit the debt is yours

- Do not include any payment

- Do not provide your Social Security number or bank information

- Do not sign with more than your printed name

- Do not agree to any payment arrangement

Professional Validation Letter Library

CDM's debt validation letter library includes professionally formatted §809(b) validation letters for every debt type, pre-built with the 12 documentation demands that make collectors prove chain of ownership. For operators, CDM tracks the 30-day window automatically across every active client file.

Access CDM Letter LibraryAffiliate link. We may earn a commission at no extra cost to you.

Figure 2: Regulation F Itemization Matrix (12 CFR §1006.34) — Shows the 5-field itemization matrix and mandatory compliance standards. Missing, blank, or inconsistent fields trigger violations. This is the framework collectors fear most.

Section 5: The Documentation Protocol — Building Your Legal Case

After the certified letter is in the mail, your job shifts from action to documentation. Every contact the collector makes after your validation request — before providing valid verification — is a potential FDCPA violation worth up to $1,000.

Day-by-Day Documentation Framework

Note the mailing date and tracking number. Create a folder (physical or digital) for everything related to this account. Save a copy of your letter.

The collector receives the letter. Note the exact date on the certified mail return receipt. This date starts the clock for their verification obligation.

Log every contact the collector makes. Date, time, phone number or sending address, what was said or written. Each contact after receipt of your validation letter — before providing valid verification — is a potential FDCPA violation.

If no verification has been provided, the collector is not merely delayed — they are in ongoing violation. The clock for their obligation does not expire. They must stop all collection activity until they either provide verification or abandon the account.

If a collector ignores a validation request and keeps collecting anyway, that is a violation of the FDCPA, and the consumer has the right to sue in federal court. The documentation of each post-validation contact is the legal case.

Section 6: What Counts as Real Validation

When the collector responds to a validation request, most consumers accept whatever they receive as valid. Most of it is not. The question "What actually constitutes sufficient validation under §809(b)?" is completely absent from every consumer guide. ScorePivot's framework provides the checklist.

Sufficient Validation Includes:

- Account statement from original creditor showing original balance and payment history

- Bill of sale or assignment agreement showing chain of ownership

- Documentation of original signed agreement (credit card terms, loan docs)

- Itemized breakdown matching Regulation F requirements

Insufficient Validation:

- A letter restating the same balance from the collector's own records

- A printout from the collector's internal database

- A letter stating "we have verified the debt" without documentation

- An affidavit from the collector's representative

If the documentation is vague or missing key details — like an original creditor's name or loan agreement — it is not considered valid proof. You can challenge the debt again or escalate the matter to the CFPB or FTC.

Even after valid verification, these rights remain: you may still dispute the amount, challenge chain of title, dispute DOFD accuracy, challenge SOL status, use FCRA §611 to dispute with bureaus, and negotiate settlement and deletion. See our Debt Buyer Playbook 2026 for tier-ranked settlement rates and deletion policies.

Section 7: After 30 Days — The Recovery Path

The most under-documented path in all of debt validation content: what consumers can do when the 30-day window has passed. Every guide tells consumers to send the validation letter within 30 days. Not one guide explains what to do after. This is the highest-volume frustrated-consumer search in this space: "I didn't send the letter in time — do I have any rights left?"

The answer is yes — substantial rights remain.

Rights That REMAIN After 30 Days

- The right to send a validation request — it just doesn't trigger the automatic §809(b) freeze

- The right to send a written cease-and-desist to stop all contact under §809(c)

- FCRA §611 bureau disputes — dispute the debt directly with the credit bureaus

- FCRA §623 furnisher disputes — dispute directly with the data furnisher

- The right to challenge accuracy of any information in the credit report

- The right to sue for FDCPA violations that occurred within the past 12 months

- State mini-FDCPA protections — often more protective than federal law

If the 30-day window has passed, the path forward involves disputing directly with the credit bureaus and the furnisher, not just the collector. The validation letter sent after 30 days can still have an impact on collection efforts — the FDCPA doesn't explicitly state what happens after 30 days, so your letter can still influence collection even without triggering the automatic freeze.

For the complete dispute strategy, see our FCRA Compliance Guide 2026 which covers §611, §623, and the full bureau dispute workflow.

Section 8: Zombie Debt and Statute of Limitations

The most underserved content overlap in all of consumer credit. Validation guides and SOL guides exist in silos. ScorePivot's framework integrates them into a unified decision framework.

The Two Clocks: SOL vs. FCRA 7-Year Reporting Period

Statute of Limitations (SOL)

The time period during which a creditor or collector can sue you to collect the debt. Varies by state: 3-10 years. After expiration, they cannot sue — but can still contact you asking for payment.

FCRA 7-Year Reporting Period

Under the FCRA, most negative items stay on your credit report for 7 years from the date of first delinquency. This clock is independent of the SOL and cannot be restarted by payment.

Critical: These two clocks operate completely independently. A debt can be past the SOL (meaning they can't sue) but still on your credit report. A debt can fall off your report but still be within the SOL for lawsuits.

The Clock-Restart Trap — The Most Dangerous Consumer Mistake

In most states, making any payment — even one dollar — on a time-barred debt restarts the statute of limitations from the date of that payment. This is the most common trap consumers fall into.

Never make a payment on old debt without understanding the consequences. The validation letter creates a formal record that no payment was made, no admission of liability was provided, and no agreement to pay was entered into. It is the protective step that prevents accidental clock restart.

Monitor for Zombie Debt Resurfaces

Time-barred debt collectors often resurface on credit reports years after they should have dropped off. Daily 3-bureau monitoring alerts you the moment any old account appears — so you can validate immediately rather than discovering it only when you apply for credit.

Start 3-Bureau MonitoringAffiliate link. We may earn a commission at no extra cost to you.

Section 9: The FDCPA Violation Menu — What You Can Sue For

If a collector violates the FDCPA, you can sue in federal or state court within one year of the violation. You can recover up to $1,000 in statutory damages per lawsuit, actual damages for financial harm and emotional distress, and attorney's fees (which the collector pays if you win). Most FDCPA attorneys handle these cases on contingency at no cost to you.

Most consumers do not know that FDCPA violations create per-violation claims. A collector who sends 5 collection letters after receiving a validation request, before providing verification, has committed 5 separate violations.

Pre-Validation Violations (§809(a) and Regulation F failures)

- Failure to send validation notice within 5 days of first contact

- Sending a deficient validation notice missing required elements

- Missing itemization or itemization date

- Delivering notice electronically without consumer consent

During Validation Period Violations (§809(b))

- Any collection contact after receiving validation request, before verification (each contact = separate violation)

- Credit bureau reporting updates to pressure the consumer

- Threatening to sue during validation period without verification

- Attempting to collect from third parties (family, employer)

General Collection Violations (The 7-in-7 Rule and More)

- Calling before 8 a.m. or after 9 p.m. consumer's local time

- Calling more than 7 times in 7 consecutive days per §1006.14 (the "7-in-7 rule")

- Calling within 7 days after having a telephone conversation about the debt

- Using threatening, abusive, or obscene language

- Threatening to sue on time-barred debt (Regulation F §1006.26(b))

Document every contact after your validation request date. Log every call, letter, and email with dates, times, and content. This documentation is the legal case. Many consumer attorneys handle these cases on contingency because the statute awards attorney's fees.

Section 10: State Mini-FDCPA Laws — Your Extra Layer of Protection

About 31 states have adopted their own laws that regulate collection practices (mini-FDCPA laws). These state laws may regulate a wider class of entities than the federal FDCPA — including original creditors collecting their own debts, which federal law does not cover.

California (Rosenthal Fair Debt Collection Practices Act)

California's Rosenthal Act now covers commercial debt up to $500,000 as of July 1, 2025. If a sole proprietor or "natural person" guaranteed a business loan, collectors can no longer use harassment, deceptive letters, or excessive calls. Critically, the Rosenthal Act applies to original creditors collecting their own debts — unlike the federal FDCPA.

New York

New York explicitly prohibits all collection activity on time-barred debt. New York City has additional disclosure requirements. NYC proposed additional rules including 45-day dispute pauses and mandatory language disclosures, though currently postponed due to litigation.

Colorado, Oregon, and Others

Colorado, Oregon, and several other states impose requirements that exceed federal Regulation F standards. Research your state's specific protections and add state law citations to your validation letters for double-layer protection.

A consumer in a high-protection state has two sets of rights to invoke simultaneously — federal FDCPA/Regulation F rights and state mini-FDCPA rights. The state rights may provide additional remedies, additional prohibited actions, and in some cases private rights of action against original creditors who fall outside federal jurisdiction.

Section 11: Electronic Communications and Regulation F

Since Regulation F legalized text and email collection communications in November 2021, collectors have been sending validation notices electronically — sometimes without proper consent documentation. If a collector delivered the original validation notice by text or email without your prior consent to electronic communications, the notice may not have been validly delivered. This means the 5-day/30-day clock may not have started.

What Regulation F Requires for Electronic Contact

- Prior consent: Consumer must have consented to receive communications at that email address or phone number

- Opt-out mechanism: Every electronic message must include a clear way to opt out

- Required disclosures: Specific language must appear in electronic validation notices

- The 7-in-7 rule for phone calls: No more than 7 calls per 7 consecutive days per debt

- Note: There is no equivalent cap for text messages under federal law — some states provide additional protection

If you received your first collection notice electronically, audit whether proper consent existed. If not, the validation clock may not have started, and you may have an independent FDCPA violation claim.

Section 12: Validation for Specific Debt Types

Medical Debt

Unique chain of custody issues. HIPAA interaction creates additional documentation requirements. Medical debt under $500 no longer appears on credit reports as of 2023. See our Medical Debt Deletion 2026 guide.

Student Loans

Federal student loans: FDCPA doesn't apply to Department of Education or servicers acting on their behalf. Private student loans: FDCPA fully applies when collected by third-party debt collectors.

Credit Card Debt

Chain of ownership documentation is the key challenge with debt buyers. Midland, PRA, LVNV, and other buyers often cannot prove they legally own purchased accounts. See our Debt Buyer Playbook 2026.

Auto Loan Deficiency

Post-repossession collection creates unique validation opportunities. The deficiency balance calculation is often challenged — request full documentation of sale proceeds and fee calculations.

Section 13: Debt Validation for Credit Repair Operators

How to structure validation services under CROA compliance. Debt validation is the first step in the professional credit repair workflow: if validation fails, the collection entry should be removed. If validation reveals errors, those errors become grounds for FCRA disputes. If validation succeeds, the path shifts to negotiated settlement with deletion.

The Professional Validation Workflow

- 1

Client Authorization

Obtain proper authorization to act on client's behalf. CROA-compliant engagement letter required.

- 2

Validation Letter Generation

Generate §809(b) validation letters with the 12-item documentation request list. Track the 30-day window.

- 3

Response Evaluation

Evaluate collector responses using the "Is This Real Validation?" checklist. Document deficiencies.

- 4

FCRA Dispute Chain

Integrate validation documentation with §611 bureau disputes and §623 furnisher disputes.

- 5

Settlement Pipeline

If validation reveals debt is valid, shift to negotiated settlement with deletion. Tier 1 buyers auto-delete upon payment.

Build Your Credit Repair Business

The Credit Hero Challenge teaches credit repair professionals how to structure validation and dispute services, generate leads, price services, and scale operations. If you're ready to turn this knowledge into a business, start here.

Start the Credit Hero ChallengeAffiliate link. We may earn a commission at no extra cost to you.

Section 14: The Scam Detection Toolkit

Phantom debt operations work by fabricating debts for amounts consumers might believe they owe. Scammers use real-sounding names and real debt amounts gleaned from data breaches. A validation letter serves two purposes simultaneously: exercising legal rights and exposing scammers.

Scammers cannot validate because they have no documentation for debts that don't exist. If a "collector" cannot produce any documentation, you may be dealing with phantom debt fraud.

Red Flags That Indicate a Phantom Debt Operation

- Cannot provide name of original creditor

- Cannot provide any account documentation

- Demands immediate payment by wire transfer, gift card, or cryptocurrency

- Threatens arrest or criminal prosecution (debt collection is civil, not criminal)

- Refuses to provide a mailing address for disputes

- The debt does not appear on any of your three credit bureau reports

If a collector cannot validate AND the debt appears fraudulent, report the operation to the FTC at reportfraud.ftc.gov and your state Attorney General's consumer protection division.

Section 15: Frequently Asked Questions

What is a debt validation letter?

A debt validation letter is a formal written request sent to a debt collector demanding they prove you owe the debt they claim. Under FDCPA §809(b), you have 30 days from receiving their initial notice to send this letter, which triggers a legal freeze on all collection activity until they provide proper documentation.

How do I write a debt validation letter?

Include your name and address, the collector's name and address exactly as shown on their letter, any reference numbers, an explicit statement disputing the debt under 15 U.S.C. §1692g(b), and a request for the 12 specific documentation items listed in Section 4. Send via certified mail with return receipt requested.

What happens if a debt collector can't validate the debt?

If a collector cannot provide valid verification, they must cease all collection activity — no calls, no letters, no credit reporting updates, and no lawsuits. If they continue collecting without validation, each contact is a separate FDCPA violation worth up to $1,000 in statutory damages.

Can I dispute a debt after 30 days?

Yes. Substantial rights remain after 30 days: FCRA §611 bureau disputes, FCRA §623 direct furnisher disputes, written cease-and-desist under §809(c), state mini-FDCPA protections, and the right to sue for any FDCPA violations within the past 12 months.

What is the difference between debt validation and debt verification?

The terms are often used interchangeably, but legally: validation refers to the consumer's right under §809(b) to demand proof. Verification is what the collector must provide in response. A form letter restating the same balance is not valid verification.

Does a debt validation letter stop collection activity?

Yes, if sent within 30 days. Under §809(b), sending a written validation request triggers an automatic freeze on all collection activity until the collector provides proper verification. Send via certified mail to create proof of receipt.

What is the 7-in-7 rule?

Under Regulation F §1006.14, a debt collector cannot call you more than 7 times within 7 consecutive days regarding a specific debt. They also cannot call within 7 days of having a telephone conversation with you about that debt.

What is zombie debt?

Zombie debt is old debt past the statute of limitations that collectors attempt to revive. Making even a $5 payment can legally restart the SOL in most states. Send a validation letter first — it creates a record that no payment was made.

Does debt validation work for credit repair?

Yes. Debt validation is the first step in the professional credit repair workflow. If validation fails, the collection should be removed. If validation reveals errors, those errors become grounds for FCRA disputes. If validation succeeds, the path shifts to settlement with deletion.

Can I send a debt validation letter by email?

The safest approach is certified mail with return receipt requested — this creates documented proof of receipt that holds up in court. While Regulation F permits electronic communications, you need proof the collector received your dispute.

Ready to Exercise Your §809(b) Rights?

The next 30 days will determine your outcome. Pull your credit reports, audit the collector's notice, and send your validation letter. The framework in this guide has helped consumers erase millions in uncollectible debt.

Affiliate links. We may earn a commission at no extra cost to you. See our disclosure.