The Week White-Collar America Realized Their Jobs Weren't Automated — They Were Eliminated

AI Layoffs 2026 — The Machine-Driven Job Crisis Creating the Greatest Credit Repair Business Opportunity in a Generation

In April 2026, tens of thousands of profitable-company employees woke up to the same email: “Your role has been eliminated as part of our AI transition.” This brief breaks down the economic shock no one is prepared for — and the counter-trend opportunity almost no one sees: the rise of the Restoration Economy and the credit-repair businesses built to serve it.

Free — no login, no credit card. Independent review. We may earn a referral, but your price stays the same.

1. The Shattered Safety Moment: Why 2026 Is Different

If you're reading this after a layoff, you're not "between opportunities." You're standing in the wreckage of an assumption that felt true your entire adult life: "If I do good work in a knowledge job, I'll be safe."

For decades, that assumption mostly held. Recessions came and went, but white-collar roles were the last to go and the first to come back. 2026 broke that pattern.

The Middle-Management Compression

What's happening right now isn't just "cost cutting." It's structural compression. Companies aren't trimming around the edges; they're hollowing out the middle:

- • Layers of coordination, review, and documentation are being handed to AI agents

- • "Good enough" outputs are suddenly "good enough" for leadership

- • Roles that sat between executives and frontline execution are being reclassified as optional

If you were in that middle band—senior enough to carry responsibility, not senior enough to set direction—you're in the blast radius. You didn't underperform. The architecture changed.

For a lot of white-collar workers, this doesn't feel like "the market turned." It feels like betrayal. You watched stock prices jump on the news of layoffs that included your name. That betrayal has side effects: you don't trust corporate messaging, you don't trust "opportunities" that sound like buzzwords, and you're hypersensitive to being sold to when you're vulnerable.

Watch: The 90-Day Credit Collapse Explained

2. The AI Layoff Wave: The Data, The Pattern, The Acceleration

Before we talk about credit repair or business models, we need to answer one question: "Is this just a rough patch, or is the ground actually moving?" The numbers say the ground is moving.

Q1 2026: The Inflection Point

78,557

Tech job cuts Q1 2026

47.9%

AI-attributed cuts

+2.7x

vs Q1 2025

This is not a one-off correction. The 2026 layoffs are explicitly architectural: companies are restructuring around AI, flattening layers, and reallocating headcount to AI-adjacent roles. If you were in customer support, operations, mid-tier engineering, or marketing—roles sitting in the overlap between "expensive human" and "good enough AI"—you weren't underperforming. You were recategorized.

Why This Matters for Your Next Move

If this were just a cyclical downturn, the rational move would be: tighten spending, ride it out, jump to a similar role at a different company. But when the architecture changes, "wait it out" stops being a strategy and starts being a slow bleed. That's why this guide talks about building something that isn't at the mercy of the next AI memo.

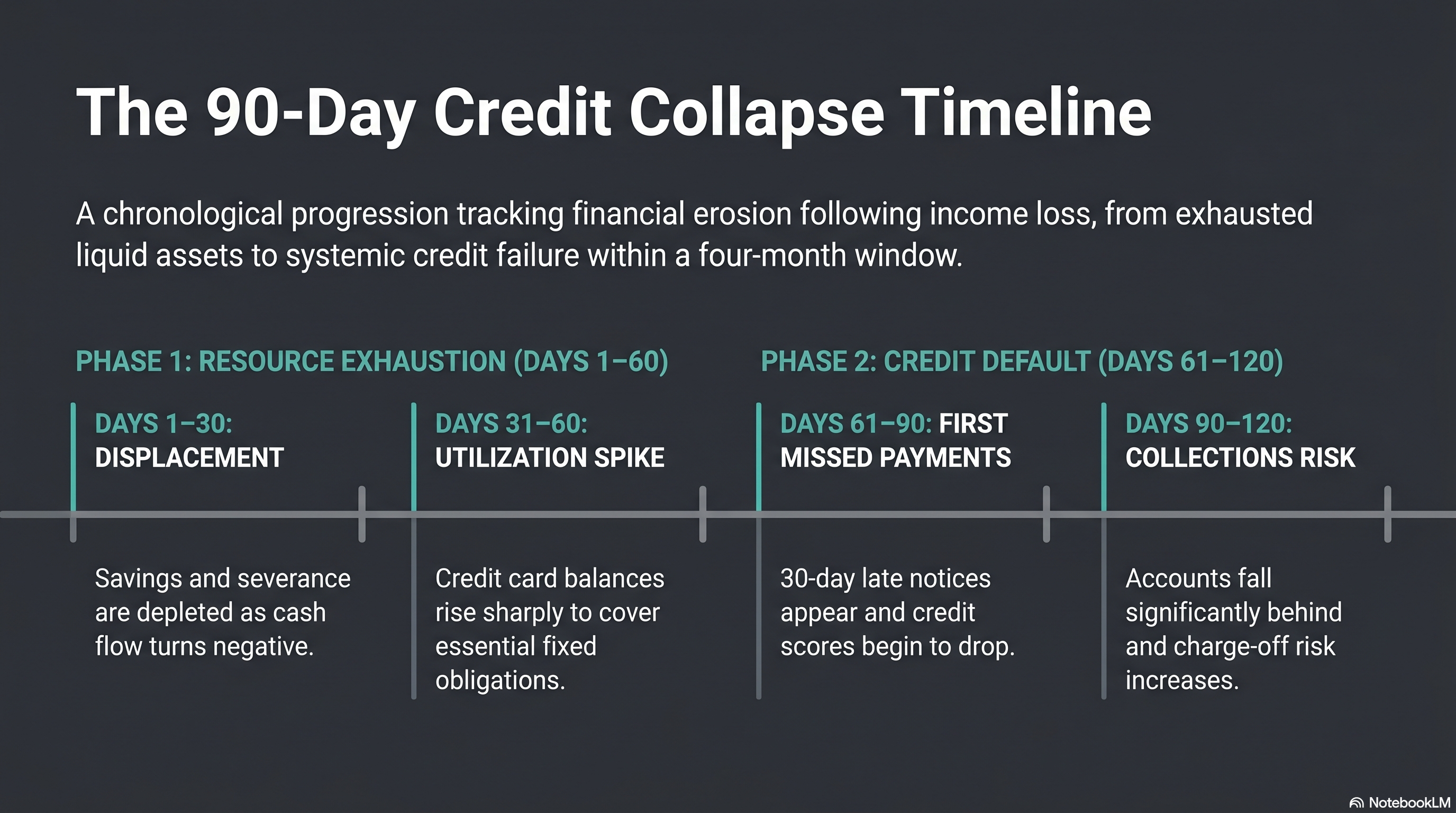

3. The 90-Day Credit Collapse: How Job Loss Turns Into Score Damage

Job loss does not immediately damage credit. There is a 60–180 day lag between displacement and credit damage. Here's the timeline:

Displacement. Worker draws savings and severance.

Savings depleted. Credit card utilization rises.

First missed payments. Score begins to drop.

Collections appear. Potential charge-offs. Score damage severe.

Worker finds new employment but credit damage persists. Repair demand emerges.

The Math for a Laid-Off Tech Worker

• Average salary: $95,000–$140,000

• Mortgage/rent: $2,800–$3,500/month

• Student loan payment (mandatory): $400–$800/month

• Car payment: $650/month

• Credit card minimum payments: $400–$600/month

Total fixed obligations: $4,250–$5,650/month. Unemployment insurance typically covers 40–60% of prior wages—meaning the newly displaced worker is immediately cash-flow negative.

Within 90–120 days, a consumer who had a 720–780 credit score and zero derogatory marks is looking at a 580–640 score with missed payments, rising utilization, and potential collections.

Watch: The 2026 Credit Crunch in 60 Seconds

This pipeline means the tsunami of Q1 2026 tech layoffs is producing a surge of credit-damaged consumers that will peak in credit repair demand precisely in Q3–Q4 2026 through 2027. But here's what most people miss: charge-off deletion strategy and FCRA 2026 dispute rules create pathways that these newly damaged consumers will desperately need.

4. The “Shocked Prime” Consumer Profile

The people being hit hardest by AI layoffs in 2026 are not the usual “credit repair” stereotype. They're not serial late-payers. They're not chronic over-spenders. They're not people who “never learned how money works.”

They're what this guide calls shocked prime — consumers who, up until 90 days ago, had 720–780 credit scores, no recent derogatories, stable income, auto-pay on everything, and had never missed a payment on purpose.

They did everything right:

- • Bought a home “within their means”

- • Financed a reliable car

- • Paid their student loans

- • Contributed to retirement

- • Kept utilization reasonable

Then AI took their job. Not because they were lazy. Not because they were incompetent. But because their role sat in the overlap between “expensive human” and “good enough AI.”

Why “shocked prime” matters for credit repair

Highly motivated — they've never been in this position before

Highly responsive — they open emails, answer calls, follow instructions

Highly referential — they tell friends, coworkers, and family when something works

They're not looking for a miracle. They're looking for a map. And that's exactly what a well-run, compliant credit repair business provides.

5. The $1.39 Trillion Debt Bubble: The Silent Credit Recession

On paper, the economy looks fine. Unemployment is “manageable.” Markets are “resilient.” Headlines say “soft landing.” But underneath that narrative, something else is happening: Americans are carrying $1.39 trillion in credit card debt at record-high interest rates.

The math problem no one can outrun

When APRs sit at 22%+, even “manageable” balances become traps. A $7,500 balance at 22% APR with minimum payments can take years to clear.

Add a layoff, and that balance doesn't go down — it goes up. Add rising utilization, and credit scores don't hold — they drop.

Layer in:

- • AI layoffs hitting high-income workers

- • Fixed obligations that don't shrink

- • Savings that evaporate in 90–120 days

You get a wave of consumers who were “fine” on paper in January, are in deep credit distress by June, and will be actively seeking credit repair help by Q3–Q4.

This is why the timing of this guide matters. You're not reading this in a vacuum. You're reading it at the front edge of a multi-year demand wave.

6. The Restoration Economy: Why Credit Repair Surges in Downturns

Every time the economy breaks, one pattern repeats: demand for credit repair surges 6–18 months later.

Foreclosures and charge-offs flooded credit reports.

Missed payments and deferred obligations came due.

High-income workers entering the same pipeline.

Credit is not just a number. It's access.

- • Access to housing

- • Access to transportation

- • Access to employment in some industries

- • Access to lower interest rates that make everything else cheaper

When that access is damaged, people don't shrug. They Google. They join Facebook groups. They look for anyone who can help them understand what's accurate, what's fixable, what's negotiable, what's deletable. That's the Restoration Economy — and credit repair sits at its center.

7. The Business Opportunity: Why Laid-Off Pros Are Ideal Operators

If you've been laid off in 2026, you might look at “starting a business” and think: “I'm the last person who should be doing that right now.” But look at what a modern credit repair business actually requires:

Systems thinking

Documentation discipline

Process management

Client communication

Basic tech comfort

Compliance orientation

If you've worked in operations, project management, customer success, marketing, product, or engineering — you already have the core skills.

You don't need to be a “salesperson,” a “guru,” or an “influencer.” You need to be: organized, ethical, and willing to follow a proven workflow.

Laid-off professionals are ideal operators because they understand documentation, respect compliance, can follow structured processes, and know what it feels like to be on the other side of the table. They're not just running a business — they're running a restoration system for people like them.

Watch: This Is Your Moment — Restoration Economy Operator

8. The Software Stack: AI Tools That Scale Credit Repair

Ten years ago, starting a credit repair business meant writing every letter by hand, tracking every client in spreadsheets, and hoping nothing slipped through the cracks. In 2026, that model is dead.

Credit Repair Cloud (CRC)

Client onboarding, dispute workflows, letter generation, status tracking, billing. The operational backbone of the modern operator.

Credit Dispute Manager (CDM)

Advanced letter logic, templates, and compliance-aligned dispute flows. Use the 609 dispute letter generator for FCRA-compliant letters.

Monitoring Partners

IdentityIQ, Aura, NordProtect: recurring revenue, live credit data, and client dashboards.

AI Assistants

For drafting emails, summarizing reports, generating SOPs, and handling FAQs. Automate the repeatable so you can focus on reviewing, deciding, and supporting.

The stack is subscription-based, workflow-driven, and documentation-heavy — built exactly for the kind of person who just got laid off from a knowledge job. You become the systems manager, not the “human printer.”

9. The Regulatory Moat: CROA, TSR, ESCRA, and the Compliance Advantage

If you've been laid off in 2026, you're already allergic to risk. You're not looking for a "side hustle"—you're looking for stability, legitimacy, and protection. This is where credit repair's regulatory environment becomes a competitive moat.

CROA: The Foundation

The Credit Repair Organizations Act requires: written contracts, disclosures, no advance fees, no false promises, and a 3-day cancellation window. This protects consumers and protects you from competing with scammers.

TSR: The Billing Guardrail

The Telemarketing Sales Rule says: if you acquire clients via telemarketing, you cannot charge until 6 months after delivering results. The modern model is monthly subscription—work performed, then billed, documented results. It's clean, compliant, and predictable.

ESCRA & The 2026 Shockwave

The proposed Ending Scam Credit Repair Act would require state licensing, increase penalties, and require proof of results. Regulation is a moat. It wipes out the scammers, shortcuts, and unregistered operators. And it leaves behind compliant operators, software-driven workflows, documented results, and audit-ready systems.

The more regulated credit repair becomes, the more valuable compliant operators become.

10. The Market Size: A Fragmented Multi-Billion-Dollar Industry With No Dominant Player

The credit repair services market, valued at USD 5.98 billion in 2026, is projected to reach USD 13.05 billion by 2032, growing at a CAGR of 13.77%. But the most important number isn't the size—it's the fragmentation.

62,000+

Firms in the market

15%

Top 4 companies combined

0%

Dominant player market share

A market where the top four players hold less than 15% combined market share is a market that rewards new, nimble operators. This is fundamentally different from search engines or social media. There is no Google of credit repair. There is no Facebook of financial recovery. The opportunity is genuinely accessible to individual entrepreneurs.

Documented Operator Success

Credit Repair Cloud has helped over 20,300 active users quit their 9-to-5, improve over 13.7 million credit report items, earn over $229 million in revenue, and helped 93 users become millionaires. These aren't hypothetical projections—they're documented, verified outcomes from real operators using the same software stack.

11. The Social Intelligence: What People Are Saying Right Now

If you want to understand a market, don't look at headlines. Look at the comments. Look at Reddit, TikTok, Facebook groups, X, Discord servers, layoff forums, and credit repair communities. The emotional pulse is unmistakable.

Reddit (r/personalfinance, r/layoffs)

"I got laid off 4 months ago and just got my first 30-day late mark. I had a 750 score. What do I do?"

This is the highest-volume thread type: laid-off tech workers, previously credit-responsible, now experiencing their first derogatory mark. Confused, scared, motivated to act. Ideal credit repair client.

TikTok (AI Layoff Content)

"AI took my job. Here's my credit score 90 days later."

These videos go viral because they're raw: screenshots, timelines, missed payments, utilization spikes, collections appearing. People aren't hiding credit damage anymore. They're documenting it.

Facebook Groups (Personal Finance)

"Should we pay the mortgage or the credit cards?"

This is the moment before collapse. Fear, shame, confusion, and urgency collide. The emotional environment your business enters.

12. The 2026 Action Plan: How to Start a Credit Repair Business Today

The reader is overwhelmed. Scared. Financially strained. Skeptical. Exhausted. So the plan must be simple, calm, step-by-step, low-risk, compliant, and doable.

Pull All 3 Credit Reports

Use IdentityIQ, Aura, or NordProtect. You need to know: what's late, what's inaccurate, what's in collections, what's about to break. This is the foundation. See your 7 fixable errors.

Assess the Damage

Look for: utilization spikes, 30-day lates, 60-day lates, collections, charge-offs, reporting errors. This is where most people realize: "I can't fix this alone."

Start Your 30-Day CRC Trial

This is the lowest-risk, highest-leverage move. You're not committing to a new career. You're exploring: a system, a workflow, a business model, a path to income. This is professional hedging—not a gamble.

Start Free 30-Day CRC TrialIndependent review. We may earn a referral benefit at no extra cost to you.

Begin Your First Dispute Cycle

CRC + CDM handle: letter generation, workflows, documentation, tracking. You handle: reviewing, approving, sending, updating clients. This is where the "systems manager" identity clicks. Use the 609 letter generator for compliance.

Build Your First Client Pipeline

Start with: friends, family, coworkers, layoff peers, local groups, online communities. You're not selling. You're helping.

Scale With Automation

Use: Charla for support, Crestani's AI Marketers Club for traffic, IdentityIQ for recurring revenue, CRC for operations. This is how you turn: a crisis → a system → a business → stability.

13. The Safety Net Close: Professional Hedging in an Unstable Economy

If you've made it this far, something important has already happened: you're no longer reading this as a "laid-off worker." You're reading it as someone evaluating options—someone trying to rebuild control in a world that suddenly feels unpredictable.

In 2026, loyalty to a single employer is not a career strategy. It's a liability. The companies that promised stability are flattening, automating, restructuring, outsourcing, replacing. And they're doing it faster than the job market can absorb.

You don't need a new employer. You need a new safety net. Not a gamble. Not a leap of faith. A hedge. A parallel path. A system you control, not one that controls you.

This is why the credit repair business model fits this moment so precisely. It is: low-risk, low-overhead, software-driven, compliance-structured, recession-resistant, counter-cyclical, and in surging demand. The 30-day CRC trial is not a commitment. It's not a pivot. It's not a reinvention. It's a test. A sandbox. A professional hedge against a job market that no longer guarantees anything.

You're not choosing a new identity. You're choosing not to be blindsided again. That's the real close. Not hype. Not pressure. Not urgency. Just clarity.

Continue Your 2026 Financial Strategy

Pay-For-Delete 2026 Guide

Success rates, collector tiers, and negotiation psychology.

LVNV Funding Removal 2026

Sherman/Resurgent update, deletion probability, settlement strategy.

Charge-Off Deletion Strategy

Accuracy challenges and reinvestigation strategies that force deletion.

FCRA Compliance Guide 2026

Your dispute rights and reinvestigation requirements.

609 Dispute Letter Generator

Generate compliant dispute letters in minutes.

7-Bureau Freeze Strategy

Complete freeze directory for all 7 bureaus with phone numbers.

Your Complete 2026 Credit Restoration Path

This AI Layoffs guide is one part of the full 2026 credit-damage prevention and business-building system. Continue strengthening your financial strategy and positioning for the Restoration Economy.

Ready to Start Your Credit Recovery?

The 30-day CRC trial is risk-free. No credit card required. No pressure. Just exploration.

Compliance & Disclaimers: This content is for educational purposes only and does not constitute legal, financial, tax, or credit repair advice. ScorePivot is not a credit repair organization under CROA. Results vary based on individual circumstances. Consult licensed professionals for personalized guidance. Affiliate links are marked.