TransUnion Credit Freeze 2026:

Unlock, Lift, Phone Numbers, and the New Security Rules

Quick Start: Freeze or Lift Your TransUnion Credit (2026)

Freeze Your TransUnion Credit

Instant online freeze using the 2026 Service Center.

Temporarily Lift Your Freeze (1-Hour Rule)

Federal law: online or phone lifts must complete within 1 hour.

Check Your Freeze Status

See if you're Frozen, Temporarily Lifted, or Unfrozen.

7-Bureau Freeze Directory

Freeze all 7 bureaus — not just the Big 3.

The PIN is gone. The platform changed. 548 million Social Security Numbers are exposed. This is the only guide that covers all of it — the 7-bureau strategy, the SSN lock layer, HPPA, OBBBA, and every phone number you need.

TransUnion 2026 — All Phone Numbers

Mail address for freeze by mail:

TransUnion · P.O. Box 160 · Woodlyn, PA 19094

Independent educational guide. Affiliate-supported, never user-funded.

Section 1

The 2026 Identity Theft Emergency: Why You Must Freeze Your Credit Now

What This Guide Covers (2026 Update)

- •How to freeze, lift, and unlock your TransUnion credit using the new 2026 rules.

- •Why the PIN is gone — and what replaces it.

- •How to avoid the 'credit lock' upsell traps.

- •The federal 1-hour lift mandate for mortgages and auto loans.

- •The complete 7-bureau freeze strategy (not just the Big 3).

- •How to fix login loops, identity graph mismatches, and verification failures.

- •How to lock your SSN with four layers of protection.

Three forces are converging. Together, they have made a credit freeze mandatory — not optional — for every adult in America.

What Most People Don't Know

Freezing TransUnion alone doesn't protect you. Telecom companies, banks, insurers, and background check systems all pull from secondary bureaus like NCTUE, LexisNexis, Innovis, and ChexSystems. If you only freeze the Big 3, you leave four open doors — and that's exactly where most identity theft happens in 2026.

1.1 The DOGE / SSA Data Exposure Crisis

The Trump administration admitted in court filings that U.S. DOGE Service members accessed and shared sensitive Social Security data without the knowledge of agency officials. A March 2026 report alleged a DOGE engineer copied the Numident database — 548 million records — to a personal thumb drive.

In August 2025, the SSA Chief Data Officer filed a disclosure alleging 300 million Americans' data was uploaded to unsupervised cloud servers. In January 2026, the Trump administration admitted in court that DOGE accessed SSA data without authorization.

The result: Social Security numbers — the single most powerful tool for identity fraud — are effectively permanently compromised. A credit freeze is now the only federally protected barrier between that data and new fraudulent accounts opened in your name.

1.2 Q1 2026: The Worst Breach Quarter in U.S. History

780

Compromises in Q1 2026

140M

Victim notices issued

166

Financial services breaches

According to the Identity Theft Resource Center's Q1 2026 data breach analysis, a data event involving Under Armour accounted for 72.7 million victim notices. SoundCloud added another 29.8 million. The Financial Services industry remained the most breached sector.

Monitoring alone is insufficient. By the time monitoring alerts you, the damage is done. A freeze stops the threat before it materializes.

1.3 Why Credit Freezes Are Now Mandatory, Not Optional

A security freeze is the only federally protected identity barrier. Under FCRA, it prohibits credit reporting agencies from releasing your credit report to open a new account — without exception for any lender who hasn't already established a relationship with you.

Why monitoring and fraud alerts are not enough:

1.4 The TransUnion Platform Shake-Up — Millions Confused

TransUnion Credit Monitoring and TrueIdentity have permanently shut down. Accounts were migrated to TransUnion Credit Essentials or Credit Premium. Legacy users can log in using the same username and password — but many never received the transition email.

Millions of consumers don't know their freeze status. They froze years ago, lost their credentials, and assume they're protected. They may not be. This guide walks through exactly how to verify — and re-establish — your freeze.

Before you do anything else:

Pull your full 3-bureau report at AnnualCreditReport.com to see what is currently exposed. Then freeze. Then execute the 7-bureau strategy in Section 5.

Section 2

The TransUnion Freeze System: What Changed in 2026

Four architectural shifts have redefined how TransUnion manages freeze requests. Most guides have not been updated. This section is the definitive 2026 record.

2.1 The PIN Is Gone �� The Most Important Update of 2026

Critical 2026 Update: You no longer need a PIN.

The 6-digit PIN has been eliminated from online freeze management. You do not need a PIN to freeze, unfreeze, or temporarily lift your credit online. Millions of guides across the internet still instruct consumers to "keep your PIN safe." That advice is obsolete.

To manage your freeze by phone, call 800-916-8800. TransUnion will verify your identity by asking for your name, date of birth, address, and Social Security number. Additional questions may be asked to confirm identity. No PIN required.

This is a massive improvement over the old system, where a lost PIN meant a complicated, slow recovery process. If you froze years ago and never wrote down the PIN — your access is no longer blocked.

2.2 The TransUnion Service Center — New Architecture

The TransUnion Service Center is the unified hub for freeze management, fraud alerts, and disputes. You can add or access your credit freeze at any time for free at the Service Center.

The system performs identity graph checks on every login — comparing your IP address, device fingerprint, and location against your profile. First-time logins from new devices may trigger additional verification steps.

If the system cannot match your current device to your existing profile, it may mandate a biometric override or deliver a one-time passcode via a secure channel before granting access.

2.3 The New Biometric Verification Layer

TransUnion has shifted toward multi-factor biometric verification for high-risk actions — including freeze lifts and new device authorizations. This is a direct response to AI-powered identity fraud that has made knowledge-based authentication questions unreliable.

Fingerprint Scanning

Mobile app interface. Liveness detection prevents spoofing.

Facial Recognition

Maps facial geometry against government ID photo.

Iris Scan

Highest-security escalation. Extremely low false acceptance rate.

2.4 The Identity Graph: Why You Get Backend-Locked

The Identity Graph is a relational database that maps your name, email addresses, device fingerprints, IP history, and birthdates. When any element mismatches — a login from a new city, a misspelled old address in your file, an SSN that appears on another account — the system locks you out and may require document submission to resolve.

This is one of the most-reported consumer frustration points in 2026. Section 9 covers the exact troubleshooting steps.

Section 3

How to Freeze Your TransUnion Credit (Step-by-Step)

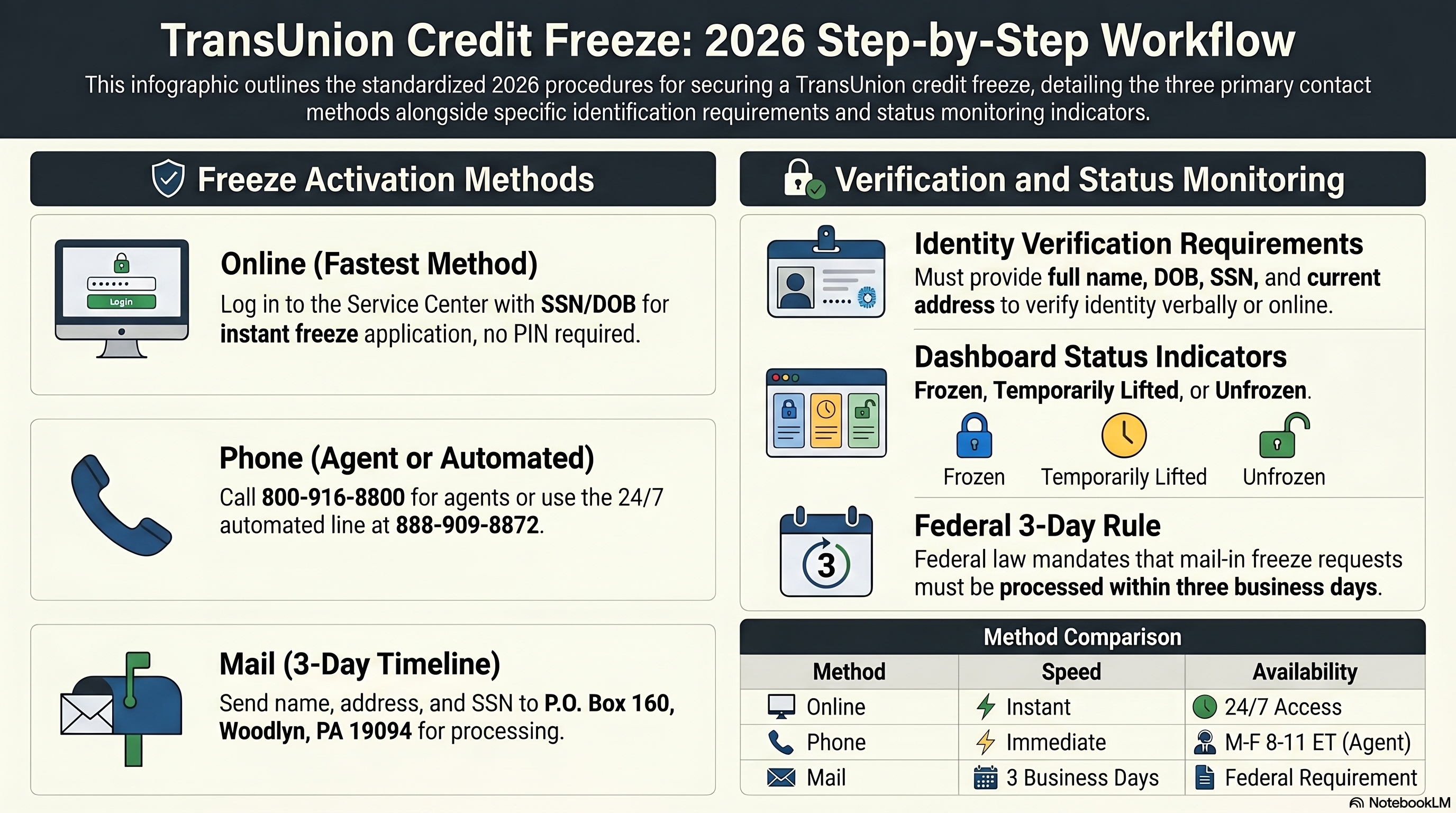

Three channels. Three timelines. One federal law behind all of them. Use the method that matches your situation.

3.1 Freeze Online — Fastest Method

Go to the TransUnion Service Center

Log in with your TransUnion account. If you had TrueIdentity or TransUnion Credit Monitoring, your same username and password still work.

Complete Identity Verification

Name, date of birth, current address, Social Security number. No PIN required. Biometric verification may be triggered on new devices.

Select Add Security Freeze

Navigate to Security Freeze in your dashboard. Confirm the request.

Verify Freeze Status

The status should update to Frozen immediately. Screenshot your confirmation.

3.2 Freeze by Phone — 800-916-8800

Call 800-916-8800. Hours: Monday–Friday 8 a.m.–11 p.m. ET · Saturday–Sunday 8 a.m.–5 p.m. ET. For 24/7 automated freeze management, use 888-909-8872.

Have ready: full name, current address, date of birth, Social Security number. The agent or automated system will verify your identity and confirm the freeze. No PIN needed.

3.3 Freeze by Mail — 3-Day Timeline

Mail your written request to:

TransUnion · P.O. Box 160 · Woodlyn, PA 19094

Include: full legal name · current address · Social Security number.

Federal law requires the freeze to be in effect within 3 business days of receipt.

3.4 How to Check If Your Freeze Is Already Active

If you froze years ago and aren't sure your freeze survived the TrueIdentity or Credit Monitoring shutdown, log in to the TransUnion Service Center and check your freeze status directly. The status will show as Frozen, Temporarily Lifted, or Unfrozen.

If you cannot access your account due to a credential mismatch, see Section 9 for full troubleshooting steps.

Figure 1: TransUnion Credit Freeze 2026 Step-by-Step Workflow — Complete reference guide showing all three freeze activation methods, verification requirements, status monitoring indicators, Federal 3-Day processing requirement, and method comparison (speed and availability).

Section 4

How to Temporarily Lift or Unfreeze Your TransUnion Report

The temporary lift is the operative skill. Master it before you need it — because needing it for a mortgage and discovering you don't know how to use it is an expensive mistake.

4.1 Temporary Lift vs. Permanent Unfreeze

Temporary Lift

Use when you need credit access for a specific window — mortgage application, car loan, apartment lease. You set the start and end date. The freeze automatically reinstates at midnight on the end date.

You can schedule up to 15 days in advance.

Permanent Unfreeze

Removes the freeze entirely. Use only when you are actively shopping for credit and expect multiple pulls over an extended period. You must manually re-freeze afterward.

Higher risk. Requires a conscious re-freeze action.

4.2 How to Lift Online

Log in to the TransUnion Service Center. Select "Temporarily Lift Freeze." Enter the date range you want the lift to be active. The lift takes effect almost immediately — but wait a few minutes before your lender initiates the pull.

To schedule a future lift: log in and set the dates for a lift up to 15 days in advance. For credit events more than 15 days away, log in closer to the date.

4.3 How to Lift by Phone

Call 800-916-8800. Verify your identity (name, DOB, address, SSN). Specify whether you want a temporary lift with dates or a permanent removal. Federal law requires the lift to take effect within one hour.

Confirm the lift timeframe with the agent before hanging up. Save any confirmation number provided.

4.4 The "Wrong Bureau" Problem — The Most Expensive Mistake

This kills mortgage applications.

The consumer lifted the TransUnion freeze. The lender pulled from Experian. The application was denied. This is the most common and most preventable freeze failure in 2026. Before any credit event, confirm which bureau your lender uses — and lift that bureau.

Ask your lender directly: "Which bureau will you pull for this application?" Then lift only that bureau. Or lift all three to eliminate the variable entirely.

4.5 The Federal 1-Hour Rule

Federal law mandates that TransUnion lift your freeze within one hour of an online or phone request. Mail requests must be processed within three business days. If TransUnion fails to meet these timelines, you have legal recourse. Document the exact time of your request and the time the lift took effect.

Section 5

The 7-Bureau Freeze Strategy — The ScorePivot Advantage

Every other guide tells you to freeze the big three and stop. That leaves six additional vectors wide open. This is the framework no competitor publishes.

5.1 Why Freezing Only 3 Bureaus Leaves You Exposed

The most-reported identity theft thread on Reddit in 2026: "I froze all three bureaus but someone still opened a T-Mobile account in my name — how is that possible?"

The answer: NCTUE. The National Consumer Telecom and Utilities Exchange is a separate bureau used by telecom providers. It is completely unaffected by your TransUnion, Equifax, or Experian freezes.

Utilities, phone carriers, banks, check acceptance services, and risk databases pull from secondary bureaus you've never heard of. A freeze at the big three protects only the credit products those three cover. See our debt validation 2026 guide on broader financial harm and why the 7-bureau strategy is non-negotiable.

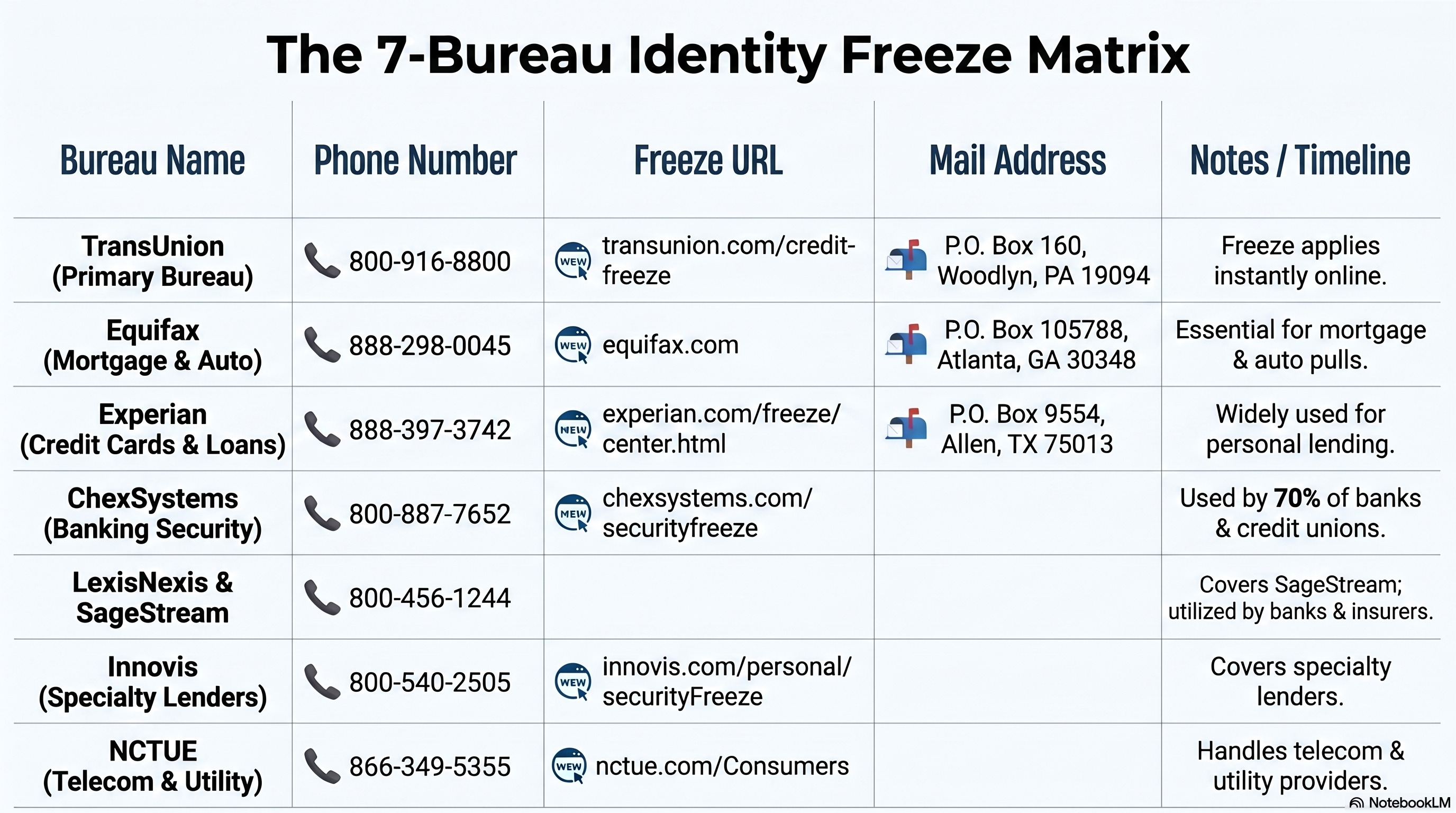

5.2 The Complete 7-Bureau Directory

TransUnion

800-916-8800Portal: transunion.com/credit-freeze

Mail: P.O. Box 160, Woodlyn, PA 19094

Primary bureau. Used by most lenders for credit decisions.

Equifax

888-298-0045Portal: equifax.com/personal/credit-report-services

Mail: P.O. Box 105788, Atlanta, GA 30348

Primary bureau. Frequently used for mortgage and auto applications.

Experian

888-397-3742Portal: experian.com/freeze/center.html

Mail: P.O. Box 9554, Allen, TX 75013

Primary bureau. Widely used for credit card and personal loan decisions.

Innovis

800-540-2505Portal: innovis.com/personal/securityFreeze

Mail: Innovis Consumer Assistance, PO Box 26, Pittsburgh, PA 15230

Fourth-largest bureau. Used by specialty lenders and screening services.

NCTUE

866-349-5355Portal: nctue.com/Consumers

Mail: N/A — online and phone only

Used by telecom, TV, and utility providers. Critical gap for most consumers.

LexisNexis (covers SageStream)

800-456-1244Portal: consumer.risk.lexisnexis.com/freeze

Mail: LexisNexis Consumer Center, Attn: Security Freeze, P.O. Box 105108, Atlanta, GA 30348-5108

Used by financial institutions and insurance carriers. A LexisNexis freeze also covers SageStream.

ChexSystems

800-887-7652Portal: chexsystems.com/web/chexsystems/consumerdebit/page/securityfreeze/placefreeze

Mail: Chex Systems, Inc. Attn: Security Freeze, 7805 Hudson Road, Suite 100, Woodbury, MN 55125

Used by 80% of banks and credit unions to screen new customers. Freeze here prevents fraudulent bank account openings.

5.3 The Telecom Gap in Detail

NCTUE focuses on payment and account history data related to telecommunications, television, and utility accounts. Major carriers — T-Mobile, Verizon, AT&T, Comcast — use NCTUE to screen new customers.

If a fraudster opens a phone account in your name and runs up charges, that collection lands on your credit report without any of the big-three protection helping you. Freeze NCTUE at 866-349-5355.

5.4 The Bank Account Gap — ChexSystems

ChexSystems is used by 80% of banks and credit unions to screen new customers. A freeze here prevents a fraudster from opening a bank or savings account in your name. This gap affects consumers who froze the big three but didn't know about ChexSystems.

Important: if you also freeze ChexSystems, you will need to temporarily lift that freeze when you want to open a new bank account yourself. The same 1-hour federal rule applies.

Figure 2: The 7-Bureau Identity Freeze Matrix — Complete 2026 contact reference guide for freezing all seven credit reporting bureaus. Includes phone numbers (24/7 availability), online freeze URLs, mailing addresses with postal codes, and coverage notes explaining which bureaus are used by lenders, banks, insurers, and telecom/utility providers.

Section 6

Freeze vs. Lock: The Distinction That Saves You Money

Credit bureaus actively push their lock products. Understanding exactly why a freeze beats a lock saves you money and gives you stronger legal standing.

6.1 Why TransUnion Discontinued Its Lock Service

TransUnion was discontinuing credit lock services across multiple platforms in early 2025. This is the defining example of why locks fail: the bureau can modify or eliminate the service at its discretion, with no federal obligation to maintain it.

Consumers who relied on a credit lock — and not a credit freeze — discovered their protection had been discontinued. A freeze cannot be discontinued. It is federally mandated.

The correct strategy:

Use the free federally-protected freeze as your foundation. Supplement with identity protection platforms like Aura or IdentityIQ for monitoring, data broker removal, and breach alerts. Never replace a freeze with a lock.

Section 7

The SSN Lock Layer: The Protection No One Talks About

A credit freeze blocks the output. An SSN lock blocks the input. No other consumer guide integrates both into a single framework. This section defines the full 4-layer identity protection stack.

7.1 E-Verify Self Lock

E-Verify is the federal system employers use to verify employment eligibility. An E-Verify Self Lock prevents your SSN from being used in any employment eligibility check — even if someone has your full Social Security number.

— Activate at: myeverify.uscis.gov

— Duration: 1 year — renewable

— Renewal reminder: 30 days before expiration

— Cost: Free

— Effect: Blocks all employment eligibility checks using your SSN

7.2 SSA Electronic Access Block

The SSA Electronic Access Block prevents everyone — including fraudsters — from accessing or changing your Social Security records online or via automated phone. This is separate from E-Verify and addresses direct SSA account manipulation.

With AI-driven voice cloning now capable of passing phone-based identity verification, this block is increasingly critical. Once activated, even if someone clones your voice and calls the SSA, they cannot access your records through the automated system.

7.3 IRS IP PIN

The IRS Identity Protection PIN is a six-digit number that must be included on your tax return. Without it, the IRS rejects the filing. Even if a fraudster has your SSN, they cannot file a fraudulent return without your IP PIN.

Activate at irs.gov/identity-theft-fraud-scams/get-an-identity-protection-pin. Renew annually. This is one of the most powerful anti-fraud tools available to consumers and one of the least-used.

7.4 The 4-Layer Identity Protection Stack

Layer 1: SSN Lock

Blocks your SSN at the government level — E-Verify + SSA Electronic Access Block

Layer 2: Credit Freeze

Blocks credit report access at all 7 bureaus — the federal barrier

Layer 3: Data Broker Deletion

Removes your data from 140+ data broker databases that feed fraudsters

Layer 4: Dark Web Monitoring + IRS IP PIN

Detects exposure and blocks tax return fraud — the final safety net

No competitor guide integrates all four layers into a single actionable framework. Most cover only Layer 2. This stack is the complete defense.

Section 8

The New Security Rules of 2026: HPPA + OBBBA

Two major legislative shifts are reshaping freeze strategy in 2026. Understanding them separates operators from bystanders.

8.1 HPPA: Trigger Leads Are Now Illegal (Mostly)

Homebuyers Privacy Protection Act — Effective March 4, 2026

Before HPPA, the moment a consumer applied for a mortgage, the credit bureaus sold that inquiry data — a "trigger lead" — to competing lenders. The consumer was immediately bombarded with calls from mortgage companies they never contacted.

Under HPPA, credit bureaus are now prohibited from selling trigger leads unless the consumer has explicitly consented. Only specific institutions — your current lender or mortgage servicer — can access your data for marketing purposes without additional consent.

Consumers who applied in Q1 2026 are still experiencing the pre-HPPA deluge and don't realize their rights changed. A credit freeze combined with HPPA protections gives mortgage applicants maximum data control. Not all lenders are complying yet — document any unsolicited contact after a credit application.

8.2 OBBBA: The New Credit Incentive System

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, introduces several provisions that directly affect credit freeze strategy in 2026.

8.3 What These Laws Mean for Your Freeze Strategy

OBBBA is generating more credit pulls. Auto loan deductions incentivize more applications. Remittance compliance requires more identity verifications. Every new credit trigger is another reason to freeze — and another reason to know exactly how to lift quickly when you need access.

The CFPB budget cut also means consumers who experience bureau errors in dispute response times will have less federal recourse. Know your state-level protections. New York's SHIELD Act, California's CCPA, and similar frameworks provide additional enforcement paths.

Section 9

Troubleshooting: The 2026 TransUnion Freeze Problems Everyone Is Having

Real-time social intelligence from Reddit, TikTok, and X reveals five active failure modes. Here is the exact resolution path for each one.

9.1 The Login Loop

Symptom: Account was created successfully, but subsequent login attempts fail with an error.

This is triggered by an identity graph mismatch — a discrepancy between the information in your file and what you entered during account creation. Common causes: a misspelled old address, a middle name discrepancy, or an SSN that appears on another file.

Resolution path:

1. Clear browser cache and cookies, then try again

2. Switch to incognito / private browsing mode

3. Try a different browser (Chrome, Firefox, Safari)

4. If the loop persists: call 800-916-8800 and request a manual identity verification

5. Have your full legal name, SSN, DOB, and current address ready

9.2 Identity Lock Re-Activating Automatically

Symptom: Submitted documents to remove an identity lock, lock re-activates after the ticket is closed.

This occurs when the underlying data mismatch that triggered the lock was not resolved by the submitted documents. The system continues flagging the same discrepancy.

Resolution path:

1. Call 800-916-8800 — do not use the online portal for this issue

2. Request to speak with a senior identity specialist, not the standard support line

3. Ask them to identify the exact data field causing the mismatch

4. If it is an address discrepancy: provide two forms of address verification (utility bill + government ID)

5. Request written confirmation that the mismatch has been resolved before ending the call

9.3 Lost Phone — MFA Crisis

Symptom: Lost or replaced phone, cannot receive MFA codes, locked out of Service Center.

Multi-factor authentication tied to a lost device creates a full account lockout. The online recovery path may be unavailable if the system cannot verify your new device.

Resolution path:

1. Call 800-916-8800 — request manual account access restoration

2. Verify identity verbally: full SSN, DOB, current address, mother's maiden name

3. Request that MFA be temporarily disabled for account access

4. Log in via computer (not mobile), reset MFA to your new device

5. Re-enable MFA before ending the session

9.4 "We Can't Show Your Freeze Status" Error

Symptom: Successfully logged in but unable to view freeze status — the dashboard shows an error instead of your freeze state.

This is a backend identity graph issue. The system authenticated your login but cannot reconcile your identity graph to display status. Often caused by the TrueIdentity migration leaving incomplete records.

Resolution path:

1. Wait 24 hours — this often resolves during off-peak hours

2. If it persists: call 800-916-8800 and ask an agent to verbally confirm your freeze status

3. If the agent cannot confirm: request escalation to the Freeze Operations team

4. Document the exact error message and the time you saw it

9.5 When TransUnion Asks You to Email Sensitive Documents

Symptom: Support requires you to email a driver's license, birth certificate, or SSN card to resolve an identity lock.

This is a real TransUnion process for high-level identity lock resolution — but also a common phishing vector. Verify before sending anything.

Verification steps before sending documents:

1. Confirm the email address ends in @transunion.com — no other domain

2. Call 800-916-8800 independently to verify the ticket number you were given

3. Ask the agent to confirm the email address they will be reviewing documents from

4. Only send via the secure upload portal if one is available — not open email

5. Document everything: ticket number, agent name, date sent

Section 10

Special Cases: Children, Incapacitated Adults, and the Deceased

These three situations require mail-only processing, additional documentation, and a higher standard of verification. No competitor covers all three. This section does.

10.1 Protected Consumer Freeze — Minors (Age 15 and Under)

A parent or guardian can place a Protected Consumer Freeze for a child aged 15 and younger. When placed, the freeze remains on the child's credit file until removal is requested. A minor can request removal themselves once they reach age 16.

With OBBBA creating government-funded Trump Accounts for newborns, protecting a child's identity from synthetic fraud from birth is now more important than ever. Fraudsters are targeting these accounts.

Mail required documents to: TransUnion · P.O. Box 160 · Woodlyn, PA 19094

Proof of Authority (one required):

— Government-issued birth certificate proving parentage

— Court-issued guardianship order

— Lawfully executed power of attorney

— Foster care certification from a county welfare department

Proof of Identity (one required):

— Social Security card or SSN

— Certified birth certificate

— Driver's license or government ID

10.2 Incapacitated Adults

A person with a valid power of attorney or court-issued guardianship order can place a Protected Consumer Freeze for an incapacitated adult. The documentation requirements are the same as for minors — proof of authority plus proof of identity for both the representative and the incapacitated individual.

All requests must be submitted by mail. Online processing is not available for this case type.

10.3 Deceased Family Members

You cannot place a traditional credit freeze on a deceased family member's file. However, you can update their credit report to show as deceased, which flags the file and prevents most fraudulent new credit inquiries.

Required to update the file as deceased: death certificate, plus the individual's legal name, Social Security number, and birth and death dates. Mail to all three primary bureaus independently.

Identity theft of the deceased is active and growing.

Fraudsters target recently deceased individuals because their credit files remain accessible for months after death. Submit the deceased notification within 30 days of death to all three major bureaus plus Innovis and LexisNexis.

Section 11

The 2026 Identity Theft Playbook: Your Action Plan

Information without a sequence is noise. This is the sequence.

11.1 Immediate Actions — Do These Today

Pull your 3-bureau report

AnnualCreditReport.com. See exactly what is on your file before you freeze. Identify every collection, every inquiry, every account you don't recognize.

Freeze TransUnion

Online at TransUnion Service Center or call 800-916-8800. No PIN needed. Verify status shows Frozen.

Freeze Equifax

equifax.com or call 888-298-0045.

Freeze Experian

experian.com or call 888-397-3742.

Get your IRS IP PIN

irs.gov/identity-theft-fraud-scams/get-an-identity-protection-pin. Prevents fraudulent tax filing even if someone has your SSN.

11.2 The 30-Day Plan

Freeze all 4 secondary bureaus

Innovis (800-540-2505) · NCTUE (866-349-5355) · LexisNexis (800-456-1244) · ChexSystems (800-887-7652). This completes the 7-bureau stack.

Activate E-Verify Self Lock

myeverify.uscis.gov. Prevents employment fraud using your SSN. Set a calendar reminder to renew in 11 months.

Activate SSA Electronic Access Block

Blocks unauthorized changes to your Social Security records online and via automated phone.

Set up dark web monitoring

Use an identity protection platform — IdentityIQ, Aura, or similar — to monitor data broker exposure and breach alerts.

Freeze for any children under 16

Mail Protected Consumer Freeze to TransUnion, Equifax, Experian, and Innovis. Include all required documentation.

11.3 The 90-Day Optimization

Audit all 7 freeze statuses

Confirm each bureau shows Frozen. Document confirmation numbers.

Audit your credit reports for accuracy

Now that the freeze is protecting you from new fraud, dispute any existing inaccuracies. Use the FCRA §611 dispute process at each bureau via the dispute letter tools. View your free reports at the free credit report checker.

Prepare your mortgage/auto freeze-lift sequence

Know which bureau your target lender uses. Know how to lift. Know the 1-hour federal timeline. Be ready to execute without delay.

Review OBBBA implications for any credit plans

Auto loan interest deduction, remittance verification, Trump Account freeze for newborns — if any apply, factor them into your freeze-lift calendar.

Start here if you have not frozen yet:

Pull your report first. Then freeze. Then execute the 7-bureau strategy.

Pull Your 3-Bureau ReportSection 12

The Operator's Path Forward

A freeze is the foundation. The complete identity protection system goes further. Here is where you go next.

12.1 What You Now Know That Most People Don't

The PIN is eliminated. Any guide that says otherwise is outdated.

Three bureaus is not enough. The 7-bureau strategy is the 2026 standard.

A credit lock is not a credit freeze. The bureau can discontinue it without notice.

The SSN lock is a separate layer. Most people have never activated it.

The 1-hour federal rule protects you. Document every request time.

The wrong-bureau lift is the #1 cause of mortgage denials among consumers with frozen credit.

TrueIdentity is gone. Verify your freeze status directly at the Service Center.

12.2 Continue Your Identity Protection Strategy

A credit freeze stops new fraud from starting. The debt validation framework handles collectors pursuing existing debts. Understanding the complete debt buyer playbook tells you exactly who is buying and reporting your accounts — and how to respond.

Debt Validation 2026

The §809(b) FDCPA framework. Force collectors to prove debts are valid — or cease collection entirely.

Debt Buyer Playbook 2026

Inside the debt buyer industry. Know who bought your debt, their policies, and how pay-for-delete works.

AI Credit Repair 2026

How AI dispute tools are outpacing manual letters — and how to use them to accelerate deletions.

12.3 Tools Referenced in This Guide

548 million records. 140 million breach victims in Q1 alone. The threat is not hypothetical.

A credit freeze is free, federally mandated, and takes ten minutes. The 7-bureau strategy adds another hour. The SSN lock adds twenty minutes.

There is no more important two hours you can spend on your financial security in 2026.

Tools to Protect Your Identity in 2026

Everything you need to execute the full 7-bureau freeze and identity protection stack in one place.

7-Bureau Freeze Directory

All seven bureaus, phone numbers, URLs, and timelines.

LaunchIdentity Theft Action Plan

Immediate, 30-day, and 90-day steps to secure your identity.

LaunchAI Dispute Letter Generator

Generate unique, compliant dispute letters in seconds.

LaunchFree Credit Reports (3-Bureau)

See your 7 fixable errors and unlock +87 FICO potential.

LaunchSSN Lock Stack Guide

E-Verify Self Lock, SSA Block, IRS IP PIN, and more.

LaunchCredit Freeze Checklist

A printable checklist for freezing all 7 bureaus.

LaunchBrian — Founder, ScorePivot

San Diego, CA

I'm Brian — the creator of ScorePivot. I keep my last name off this site not out of secrecy, but because ScorePivot isn't built on personality. It's built on precision. Every strategy, workflow, and product decision runs through me, supported by a private stack of advanced AI systems that accelerate development, strengthen compliance, and help us ship updates at a pace traditional software companies can't match. Human oversight. Machine acceleration. Zero shortcuts.